Markets tell stories. But capital flows tell them faster. In voice AI funding, the capital flow over the past two few has been unusually clear.

The numbers

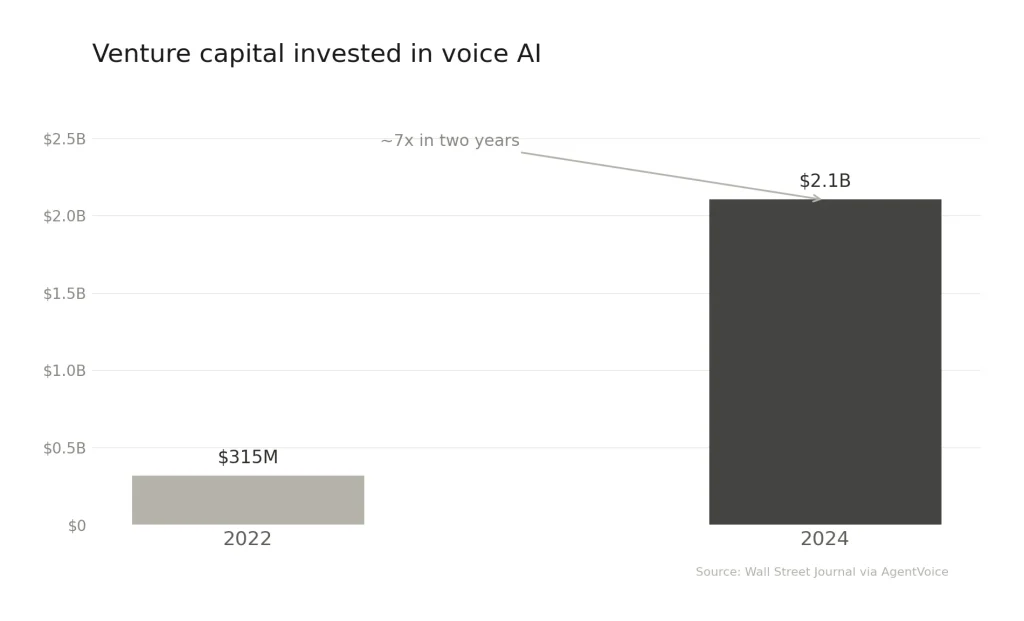

According to The Wall Street Journal, venture capital directed at voice AI totalled roughly $315 million in 2022. By 2024, that number had reached approximately $2.1 billion, a nearly sevenfold increase in two years [1]. CB Insights reported that voice AI solutions attracted $2.1 billion in equity funding in 2025 alone [2]. The pace hasn’t slowed.

Among the most prominent rounds: ElevenLabs raised $180 million in a Series C in January 2025 at a $3.3 billion valuation, co-led by a16z and ICONIQ Growth [3]. Less than a year later, in February 2026, the company closed a $500 million Series D led by Sequoia Capital, tripling its valuation to $11 billion [4]. By that point, ElevenLabs reported $330 million in annual recurring revenue, with enterprise clients including Deutsche Telekom, Revolut, and the Ukrainian government [4].

Deepgram followed a similar trajectory. In January 2026, the speech-to-text and voice AI infrastructure provider raised $130 million in a Series C at a $1.3 billion valuation [5]. The company was already cash-flow positive and serving more than 1,300 organisations before the raise [5]. Platform startups raised smaller but strategically important rounds: Vapi secured $20 million for its developer-focused voice agent platform [6], while Cartesia raised $91 million at Series A for ultra-low-latency voice models [7].

Big tech is buying, not just building

The funding story isn’t only about startups raising capital. It’s also about acquisitions.

In July 2025, Meta acquired PlayAI, a voice AI startup that had raised $21 million from Y Combinator, 500 Global, and Kindred Ventures [8]. The entire 35-person team joined Meta, reporting to Johan Schalkwyk, a former Google speech researcher who had recently joined Meta from Sesame AI [8]. Meta’s internal memo described PlayAI’s work as a “great match” for its roadmap across AI Characters, Meta AI, wearables, and audio content creation [9].

This matters because it signals that big tech views voice synthesis and voice agent capabilities as core infrastructure, not features to be licensed from third parties. When companies with the resources of Meta start acquiring voice startups, it tells you the technology has moved past experimental.

What the money actually signals

Three patterns stand out.

First, the shift from infrastructure to applications. Early funding in voice AI went primarily to model builders and API providers. Now, capital is moving up the stack. a16z observed this in their 2025 update, noting the transition from infrastructure to application layer, where voice becomes “the wedge, not the product” [10]. Investors are looking for companies that solve specific business problems with voice, not just companies that build better speech models.

Second, round sizes are inflating rapidly. Among conversational AI startups whose last round came in 2025 or 2026, the median round size exceeded $100 million, roughly triple the median for companies that last raised before 2024 [7]. That’s partly driven by the capital intensity of training voice models, but it also reflects growing confidence that these companies can build real, recurring revenue.

Third, strategic investors are joining. Deepgram’s Series C included Twilio, ServiceNow Ventures, SAP, and Citi Ventures [5]. ElevenLabs’ earlier rounds brought in Deutsche Telekom, HubSpot Ventures, and RingCentral Ventures [3]. Enterprise software companies are positioning themselves alongside the voice AI providers they expect their customers to use.

What to take from this

The capital flowing into voice AI is substantial and accelerating. But the more interesting signal isn’t the total dollar amount. It’s the composition. When strategic investors from telecommunications, CRM, and enterprise software show up in funding rounds, and when a company like Meta acquires a 35-person voice startup, the market is telling you that voice AI is transitioning from interesting technology to business infrastructure.

For companies evaluating voice AI, that’s a relevant signal. The ecosystem is maturing, the tooling is improving, and the providers are increasingly well-capitalised. The window where voice AI was too early for serious enterprise adoption is closing.

Sources

[1] AgentVoice, “AI voice in 2025: Mapping a $45 billion market shift.” September 2, 2025. Citing Wall Street Journal data. Link

[2] VoiceAIWrapper, “Voice AI Market Analysis 2026 — Trends & Growth.” March 2026. Citing CB Insights data. Link

[3] ElevenLabs, “Series C Announcement.” January 30, 2025. Link

[4] ElevenLabs, “Series D Announcement.” February 4, 2026. Link

[5] Deepgram, “Deepgram Raises $130M Series C at $1.3B Valuation to Power the Voice AI Economy.” January 13, 2026. Link

[6] Vapi, “Vapi Raises $20M to Serve Explosive Demand for Voice AI.” December 11, 2024. Link

[7] New Market Pitch, “Top Conversational AI Startups by Fundraising (2026).” March 2026. Link

[8] TechCrunch, “Meta acquires voice startup Play AI.” Anthony Ha. July 13, 2025. Link

[9] Bloomberg, “Meta Acquires Voice AI Startup PlayAI, Continuing to Add Talent.” July 11, 2025. Link

[10] Andreessen Horowitz (a16z), “AI Voice Agents: 2025 Update.” Olivia Moore. January 2025. Link